What is Financial Reconciliation? A Practical Guide for Accuracy

Think of financial reconciliation as the moment of truth for your business's finances. It’s the process where you carefully compare the financial records you keep in-house—like your general ledger—against external statements from places like your bank or credit card companies.

It’s not so different from checking your personal shopping receipts against your monthly bank statement to make sure everything adds up. The goal is simple but crucial: to ensure the financial picture you have is 100% accurate, leaving no room for doubt.

The Core of Financial Clarity

Let's use an analogy. Your business’s accounting software, whether it’s Xero or QuickBooks, holds your version of financial events—every pound you've earned and spent. Your bank statement, on the other hand, is the bank's official record of those same events. Financial reconciliation is when you sit down with both "stories" and make sure they match, line by line.

This isn’t just about ticking boxes and finding the odd mistake. It’s about achieving absolute certainty. It's the step that confirms the money you think you have in the bank is the money you actually have. Without it, you're essentially running your business on a set of well-intentioned assumptions, not hard facts.

More Than Just Balancing the Books

At its heart, reconciliation is a fundamental health check for your business. It performs a few vital functions that go way beyond simple accounting tidiness. When done right, it helps you:

- Get a True Picture of Your Cash Flow: You’ll know exactly how much cash is coming in and going out, which is the bedrock of smart spending and investment decisions.

- Spot Fraud and Errors Early: An odd transaction or a recurring discrepancy could be the first warning sign of fraudulent activity or a persistent bank error that’s quietly costing you money.

- Keep Your Financial Statements Accurate: Your balance sheet and income statement are only as good as the data feeding them. Reconciliation is what gives them integrity.

- Stay Compliant with HMRC: For filing accurate VAT and Self-Assessment tax returns, clean and reconciled books are non-negotiable. It’s your best defence against potential penalties.

The Reality for UK Small Businesses

For many UK small business owners, the reality of reconciliation is a painful monthly grind. You're trying to track down receipts sent via WhatsApp, fish out invoices from email chains, and then spend hours manually matching everything to your bank feed. This is especially true for freelancers and sole traders, where HMRC's rules mean that inaccurate records can lead to serious headaches and penalties.

To get a sense of the sheer volume of transactions happening daily, it's worth looking at the UK's payment and settlement statistics. Each one of those movements needs to be accounted for somewhere.

Financial reconciliation transforms your financial data from a collection of recorded transactions into a verified, trustworthy foundation for strategic decision-making. It’s the difference between guessing and knowing.

To sum it up, here’s a quick overview of what the process involves.

Financial Reconciliation at a Glance

| Component | Description | Business Impact |

|---|---|---|

| Internal Records | Your company's books (e.g., general ledger, cash book). | This is your version of the financial story. |

| External Statements | Official records from banks, credit card companies, or vendors. | This is the third-party version of the story. |

| The Comparison | Matching transactions between internal and external records, line by line. | Identifies discrepancies, missing entries, and timing differences. |

| The Outcome | An adjusted and verified set of financial records that are accurate. | Provides confidence in financial reports, cash flow, and tax filings. |

Ultimately, understanding what financial reconciliation is means seeing it as the guardian of your company's financial integrity. It’s a disciplined habit that provides the clarity you need to manage your cash, plan for growth, and run your business with confidence.

Why Accurate Reconciliation Is a Business Superpower

Think of financial reconciliation as less of an admin chore and more of a health check for your business finances. It might feel like you're just looking back at what's already happened, but its real power is in shaping what you can do next.

First and foremost, clean, reconciled books are your best line of defence for HMRC compliance. When it comes to filing your VAT and Self-Assessment tax returns, accurate records are non-negotiable. Getting this right helps you steer clear of stressful audits and potentially hefty penalties. But the perks go far beyond just keeping the tax authorities happy.

Unlocking Strategic Insights

Diligent reconciliation gives you a crystal-clear, real-time snapshot of your cash flow. It’s this financial clarity that allows you to stop guessing and start making truly confident decisions.

- Confident Growth: Thinking about investing in that new piece of equipment? Wondering if you can afford to hire another team member? Reconciled accounts provide the hard data to back up these big moves, turning a risky punt into a calculated decision.

- An Early Warning System: That tiny discrepancy that seems like nothing could be the tip of the iceberg. Catching a small, recurring bank error early might save you hundreds of pounds over a year. More importantly, it can expose unauthorised transactions or even fraud before real damage is done.

For accountants, this is where they can really show their value. Instead of getting bogged down in fixing data entry errors and chasing up missing paperwork, they can focus on giving you high-level strategic advice. Clean books mean they can spot trends, forecast your cash flow, and help you build a more profitable business. You can explore how Snyp's integration with Xero streamlines this foundational work, freeing up valuable time for everyone.

Reconciliation isn’t about staring in the rearview mirror. It’s about building a solid financial foundation so you can look ahead with confidence, knowing exactly where you stand.

This process is a vital safeguard against the kind of financial chaos that can quickly sink a new business. The principle applies at every scale. In the UK, major compliance schemes rely on it to align sales and payments. For example, in the Voluntary Scheme for Branded Medicines, aggregate sales of £11,805 million were reconciled to produce payments of £2,459 million. For a small business owner, the principle is identical—it’s about making sure every single pound is accounted for. You can discover more about the scale of these reconciliation efforts from GOV.UK.

The True Cost of Inaccuracy

Putting reconciliation on the back burner is like navigating without a map. An unreconciled set of books is built on assumptions, and those assumptions can lead to disastrous errors in judgement.

You might think you have enough cash to cover this month's payroll, only to be caught out by a few large payments that hadn't cleared yet. Or you could be missing out on claiming legitimate business expenses simply because the receipts were never matched to the transactions. Each month you skip adds another layer of fog, making it almost impossible to get a true picture of how your business is actually performing.

Ultimately, consistent financial reconciliation delivers peace of mind. It validates your numbers, protects you from nasty surprises, and gives you the reliable information you need to steer your business toward healthy, sustainable growth.

Your Step-by-Step Reconciliation Playbook

Now that we’ve covered the why, it’s time to get into the how. Financial reconciliation can feel like a mammoth task, but if you break it down into a clear, repeatable process, it’s far less intimidating. Think of it less like an unsolvable puzzle and more like a simple checklist.

This walkthrough is all about practical, straightforward steps. We’ll go from gathering your documents to making those final, satisfying adjustments that bring your books into perfect harmony.

Step 1: Gather Your Financial Documents

First things first, you can't compare anything until you have all your records in one place. Getting organised at this stage will save you a world of headaches later on.

You’ll need to pull together two main sets of documents:

- Internal Records: This is your side of the story. It includes your general ledger, cash book, and any reports from your accounting software (like Xero or QuickBooks).

- External Statements: These are the official records from the bank. You’ll need your bank and credit card statements for the period you’re reviewing.

Don't forget to grab all the relevant receipts and invoices for the period, too. These are the proof behind the numbers you’ve entered into your books.

Step 2: Compare Transactions Line by Line

This is where the real work begins. Get your accounting software open on one screen and your bank statement on another. The goal here is to methodically tick off every single transaction that matches.

Start by checking that the opening balance in your books matches the opening balance on your bank statement. From there, go through each entry one by one, matching items that appear on both lists. Modern accounting software is great at automating a lot of this, but you still need to cast a human eye over it to catch anything the system might have missed.

As you go, you’ll start noticing transactions that are on one list but not the other. These are your reconciling items. Don't panic when you find them; they're a completely normal part of the process and are exactly what we're looking for.

Step 3: Identify and Flag Discrepancies

After you’ve matched all the easy ones, you'll have a list of leftovers. These are your discrepancies, and they usually fall into a few common categories.

It helps to group these unmatched items to figure out what's causing the imbalance. You’ll typically find things like:

- Outstanding Cheques or Payments: You've recorded a payment, but the recipient hasn't cashed the cheque yet, or the transaction is still pending.

- Deposits in Transit: You've logged income from a customer, but the deposit hasn't cleared the bank and appeared on your statement.

- Bank Charges and Fees: The bank has taken its monthly service fees or transaction charges, which you haven't yet recorded in your books.

- Human Error: It happens to the best of us. A simple typo, like entering £54 instead of £45, is a classic culprit behind reconciliation woes.

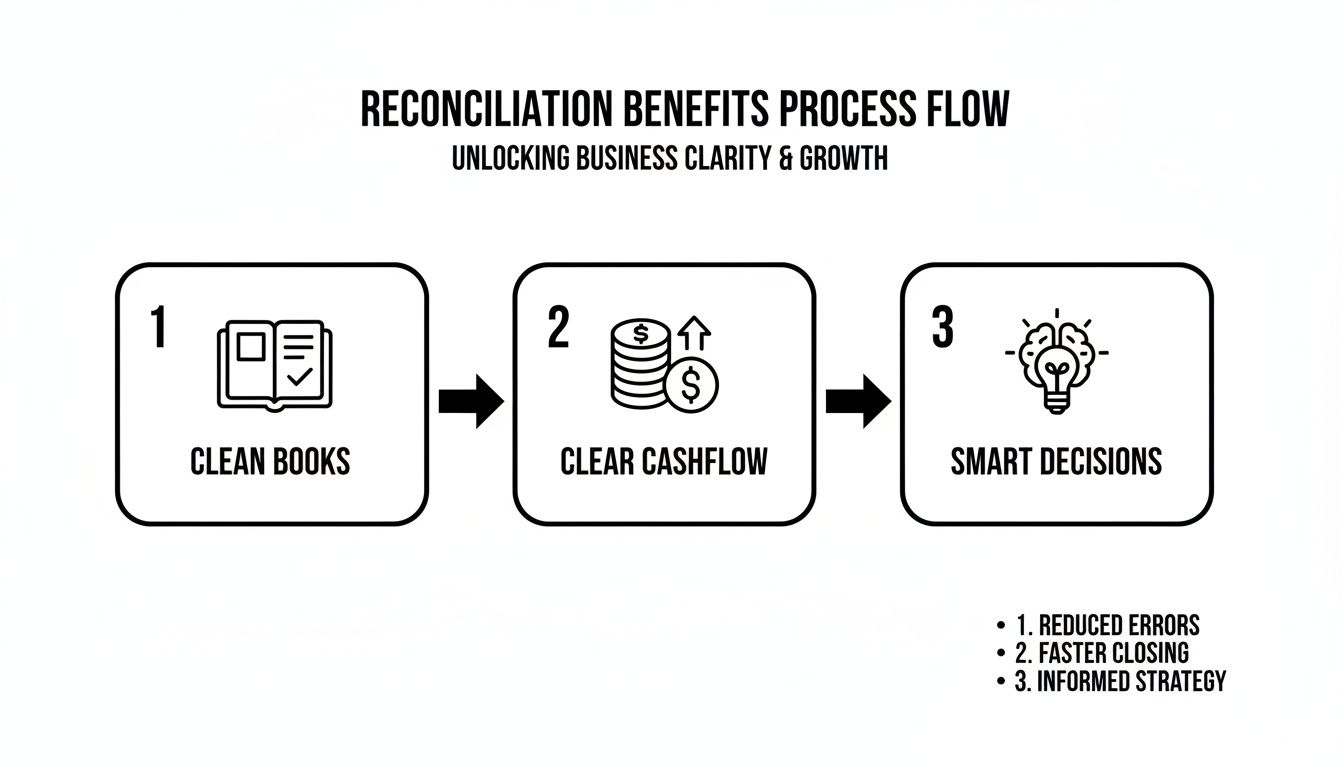

This simple flow chart shows how this structured process turns messy data into genuinely useful business insights.

The image drives home a key point: clean books lead directly to a clearer view of your cash flow, which in turn helps you make smarter decisions.

Step 4: Investigate and Make Adjusting Entries

With your list of discrepancies in hand, the final step is to investigate each one and make the necessary adjustments in your accounting records. This is the moment you bring your books back into alignment with reality.

For things like bank fees or interest, you’ll create a new journal entry to record them. For an outstanding cheque, you don't need to adjust your books, but you’ll make a note of it in your reconciliation report so you know it should clear next month. If you’ve found a simple data entry error, you just need to go in and correct it.

The whole point of an adjusting entry is to make sure your financial statements give a true and fair view of the company's financial health at the end of the period. It's the final touch-up that makes your records perfect.

Once all your adjustments are in, the closing balance in your accounting records should match the closing balance on your bank statement down to the last penny. When it does, congratulations – you’ve successfully reconciled your accounts.

For a deeper look into this specific area, you can learn more about bank statement reconciliation in our detailed guide. This structured approach turns what could be a chaotic task into a manageable and empowering routine.

Common Reconciliation Headaches and How to Cure Them

Financial reconciliation sounds simple enough on paper. In reality, it often feels more like detective work, but with fewer clues and a lot more frustration. Every business owner and accountant knows that sinking feeling when the numbers just refuse to line up.

These challenges aren't just annoying; they're a massive drain on time and can hide serious financial risks. The path to balanced books is rarely a straight one. It’s usually littered with maddeningly common obstacles, from a lost coffee receipt to a tiny data entry mistake that throws everything off.

Ignoring these issues is a recipe for disaster. Accurate reconciliation is the unsung hero that keeps small businesses afloat. Think about this: in England and Wales, 21 bankruptcies and 124 Debt Relief Orders happen every single day. In just one 12-month period, 119,046 individuals (that's 1 in every 405 adults) became insolvent. These aren't just abstract numbers; they're a stark reminder of what can happen when financial control slips, often starting with small but persistent reconciliation failures. You can dig deeper into these figures with the latest UK insolvency statistics.

Let's break down the most common culprits and, more importantly, how to fix them for good.

The Chaos of Missing Receipts

Easily the biggest headache is the dreaded missing receipt. A team member fills up with fuel, a client lunch is paid for with cash, or an online subscription renews automatically. The money is gone, but the proof of purchase is nowhere to be found, leaving an orphaned transaction on the bank statement.

This isn't just untidy bookkeeping; it's a serious compliance risk. Without a valid VAT receipt, you can't reclaim the VAT, which means you're leaving money on the table.

- The Fix: Ditch the shoeboxes and faded thermal paper. The only real solution is a strict, real-time receipt capture system. Tools like Snyp empower your team to simply snap a photo of a receipt or forward an email invoice the second a purchase is made. This creates an instant digital trail, making lost paperwork a thing of the past.

The Tyranny of Manual Data Entry

No matter how careful you are, humans make mistakes. When you're manually typing long strings of numbers day in and day out, it's inevitable. Transposing digits (typing £89 instead of £98) or misplacing a decimal point can throw your entire reconciliation into chaos.

These seemingly tiny errors are incredibly time-consuming to hunt down and can have a surprisingly big impact on your financial reports. The problem snowballs, turning a quick monthly check into a forensic accounting nightmare.

The best cure for human error is to take the human out of the equation for repetitive tasks. Let technology handle the data extraction, freeing up your expertise for what really matters: analysis and strategy.

The Trouble with Timing Differences

Another common source of confusion is timing. You record a client payment in your books on the 30th of the month, but it doesn't actually clear the bank until the 2nd of the next month. This isn't an error, but it does create a temporary mismatch that needs explaining.

Common examples include:

- Outstanding Cheques: You’ve sent a payment, but the recipient hasn’t cashed it yet.

- Deposits in Transit: You’ve banked customer payments, but they are still being processed.

The Fix: This all comes down to good documentation. Your accounting software should let you flag these items as "uncleared." During reconciliation, you simply identify them as valid reconciling items that will sort themselves out in the next cycle. Regular, monthly reconciliation makes these timing issues easy to spot, track, and manage.

To help you stay ahead of these issues, here’s a quick-reference guide to the most frequent reconciliation problems and how to prevent them.

Common Reconciliation Problems and Their Solutions

| Common Problem | Business Impact | Preventative Solution |

|---|---|---|

| Missing Receipts | Inability to claim VAT, inaccurate expense tracking, compliance risks. | Implement a digital receipt capture tool like Snyp for real-time submission. |

| Manual Data Entry Errors | Inaccurate financial reports, wasted time hunting for tiny discrepancies. | Use automation software to extract data from receipts and invoices, minimising human touchpoints. |

| Timing Differences | Mismatches between your books and bank statements, causing confusion. | Perform reconciliations regularly (at least monthly) and use your accounting software to track "uncleared" transactions. |

| Duplicate Transactions | Overstated expenses or understated revenue, leading to poor financial decisions. | Use software that flags potential duplicates for review before they are permanently recorded. |

| Bank Fees & Charges | Unrecorded bank fees create small, persistent discrepancies that are easy to miss. | Set up bank feeds that automatically import all transactions, including fees, directly into your accounting system. |

By tackling these headaches with proactive systems and the right tools, you can transform financial reconciliation. It stops being a stressful, reactive chore and becomes a smooth, predictable, and even empowering part of your financial routine.

How Automation Transforms Financial Reconciliation

If you’ve ever felt the pain of manual reconciliation, you’ll know that moving to automation isn’t just an upgrade—it’s a complete game-changer. Automation takes the most tedious, error-prone parts of the process off your plate and hands them over to smart technology. This frees you and your team to focus on what really matters: analysis and strategy.

This isn't about just scanning a document. A modern approach creates a seamless pipeline of information, flowing from the point of purchase straight into your accounting system. It turns a multi-step chore into a quick, simple review. Think of it as the difference between digging for data with a shovel and having it delivered, perfectly organised, right to your doorstep.

Beyond Scanning to Intelligent Data Capture

The first big shift is how data gets into your system in the first place. The old way involved someone physically typing details from a receipt into a spreadsheet or accounting software. Modern tools, however, use intelligent data capture that understands the context of a document, not just the characters on it.

Let's say an employee buys fuel for a company vehicle. Instead of stuffing a crumpled receipt into their wallet, they just forward the email confirmation or a WhatsApp picture to a system like Snyp. The tech instantly gets to work, extracting the key details:

- The Merchant: It identifies "Shell" or "BP" as the vendor.

- The Date and Time: It records precisely when the transaction happened.

- The Amount: It captures the total cost, splitting out the VAT.

- The Category: It knows to code the expense as "Travel" or "Fuel."

This isn't just guesswork. The process is powered by AI that learns and gets smarter over time, making sure that data is not only captured but also categorised with impressive accuracy. The result? Structured, reconciliation-ready data flows directly into platforms like Xero or QuickBooks without a single keystroke. To get a deeper sense of how this works, it’s worth looking into guides on accounts payable automation software.

The visual clarity you see in modern dashboards is a direct result of this automation. It gives you a real-time, at-a-glance view of your expenses, wiping out the usual administrative lag.

From Manual Matching to One-Click Review

When your data enters the accounting system this cleanly, the act of reconciliation itself is transformed. The painful task of manually ticking off dozens or hundreds of lines on a bank statement against your ledger simply disappears.

Instead, your accounting software’s bank feed sees a transaction come in and often finds a perfect match already waiting for it—that beautifully coded expense entry created by the automation tool. The whole process is no longer a painstaking investigation; it’s a simple validation.

Automation transforms financial reconciliation from a forensic accounting exercise into a straightforward review. Your role shifts from data entry clerk to financial supervisor.

Your new workflow becomes a simple one-click confirmation. The system flags a proposed match, and all you need to do is click "OK." This isn't just about saving a few minutes here and there. Studies have shown that automation can cut the time spent on these tasks by over 70%, freeing up countless hours for more valuable work.

The Tangible Outcomes of Automated Reconciliation

Bringing automation into your workflow delivers powerful, measurable benefits that directly impact your bottom line and operational fitness. It’s not just about convenience; it’s about building a more resilient and informed business.

Here are the key outcomes you can expect:

- Massive Time Savings: All those administrative hours once lost to chasing receipts, typing in data, and fixing mistakes are reclaimed. This allows you or your accountant to focus on financial planning, cash flow analysis, and growth strategies.

- Near-Zero Error Rates: By taking manual data entry out of the equation, you eliminate the risk of human errors like typos or transposed numbers. This leads to cleaner books, more reliable financial reports, and stress-free audits.

- Real-Time Financial Visibility: Because data is captured and coded instantly, your financial records are always up to date. You no longer have to wait until month-end to get a clear picture of your financial position. This empowers you to make sharp, data-driven decisions with the most current information available.

Ultimately, automation turns reconciliation from a dreaded, backward-looking chore into a seamless, forward-looking process. It gives you the accurate, real-time data you need to run your business with confidence and clarity.

Got Questions About Financial Reconciliation? Let's Get Them Answered

We’ve covered a lot of ground on what financial reconciliation is and why it’s so critical. But as with anything in business, the real questions pop up when you start applying the theory to your own situation.

Let's dive into some of the most common questions I hear from small business owners. Think of this as the practical, no-nonsense part of the guide.

How Often Should I Reconcile My Accounts?

For most small businesses and freelancers in the UK, the answer is simple: monthly. This is the gold standard for a reason. It’s frequent enough to catch errors before they spiral out of control, but not so often that it becomes a soul-crushing chore.

A monthly reconciliation keeps your finger on the pulse. It ensures you have accurate figures ready for VAT returns, management accounts, and making smart decisions about your cash flow. It’s all about staying in control.

Of course, there are exceptions. If you’re running a business with a huge number of daily transactions—think a busy high street coffee shop or a booming e-commerce site—waiting until the end of the month can feel like climbing a mountain. In that case, switching to a weekly reconciliation is a smart move. It breaks the work down and gives you much tighter control over your finances.

What’s the Difference Between Bookkeeping and Reconciliation?

This is a great question, and it's easy to get the two mixed up. They’re closely related, but they play very different roles.

Bookkeeping is the day-to-day job of recording every financial transaction your business makes. It’s the process of logging every sale, every purchase, every payment, and every receipt into your general ledger.

Put it this way: Bookkeeping is like writing the first draft of your company's financial story. You're capturing the plot points—the transactions—as they happen.

Financial reconciliation, on the other hand, is the editing and proofreading stage. It’s where you take that story you’ve written in your books and compare it, line by line, against an official source like your bank statement. It’s the critical step that confirms your story is factually correct.

Can I Do Financial Reconciliation Myself?

Absolutely! Plenty of sole traders and small business owners handle their own reconciliation, especially in the early days. Modern accounting software from providers like Xero or QuickBooks has made the process far more straightforward than it used to be.

But here’s the reality check: as your business grows, so does the number of transactions. What was once a quick job can easily become a major time-sink, and the risk of a costly mistake goes up, too.

This is often the point where bringing in a professional accountant or bookkeeper makes perfect sense. They have the expertise to spot and sort out complex issues quickly. A great middle-ground is to use an automation tool. By getting a tool to do the mind-numbing work of receipt capture and data entry, you make the whole process simpler for you to review, or you make it much faster (and cheaper) for your accountant to handle.

What Are Some Common Reconciling Items?

"Reconciling items" is just the technical term for the things that cause a temporary mismatch between your books and your bank statement. Finding them is the whole point of reconciliation, and they are completely normal.

Here are the usual suspects you’ll come across:

- Outstanding Cheques: You’ve written a cheque and recorded it as spent, but the person you gave it to hasn't cashed it yet. So, the money is gone from your books, but it's still sitting in your bank account.

- Deposits in Transit: You’ve received payments from a customer (especially at the end of the month) and recorded them in your accounts, but the money hasn't physically cleared and landed in your bank yet.

- Bank Charges or Fees: Your bank will take its monthly service fees or transaction charges straight out of your account. You won’t know about them until you see your statement, so you’ll need to add them to your books.

- Interest Earned: On the flip side, if your account earns interest, the bank will add it automatically. This is income that you need to record in your books to make everything match up.

Spotting and correctly accounting for these items is how you get your accounts to balance perfectly. It shines a light on those timing differences and unrecorded bits and pieces that are a natural part of doing business.

Ready to eliminate the biggest reconciliation headache of all—manual data entry? Snyp uses AI to automatically capture and categorise every receipt from your email or WhatsApp, syncing it directly to your accounting software. Stop chasing paperwork and start saving hours. Try it for yourself and see how simple reconciliation can be at https://snyp.ai.